We are now through the third quarter of 2015 and the overall housing market continues to move at a steady and positive pace with buyer interest as strong as the fall of 2014. The overall economic news remains good as well, with Michigan leading the Midwest in terms of economic growth. The combination of steady job growth, low interest rates, increasing household income, and home values give consumers increasing confidence in housing.

The housing recovery has been surprisingly strong considering so many homeowners have been sitting on the sidelines waiting for their home equities to rise, and with For Sale inventories so low, waiting for a home to purchase. With home values up, it appears that those homeowners are finally beginning to act, increasing the number of homes for sale, which in turn, should bring more buyers into the market, providing fuel for the 2016 housing market. Add to that the credit easing up for first time home buyers, (and their desire to move out of their parent’s basement) and it looks like a steady flow of buyers entering the market for the balance of this year and into 2016.

We do anticipate that For Sale inventories will be rising faster than sales, which will give buyers more choices and sellers more competition. At the same time, sellers will see increased time on the market, as well as a leveling out of home values. The charts below confirm these trends across all price categories.

Going into the fall and winter markets, sellers should be wary of over-pricing. Values are rising but not as fast, and in fact, most of the current inventory, particularly over $400,000, is over-priced compared to homes on the market this past spring. With more listings coming on the market, values may settle a little and homes that might be just a little over the market now, will be quite a bit over this winter.

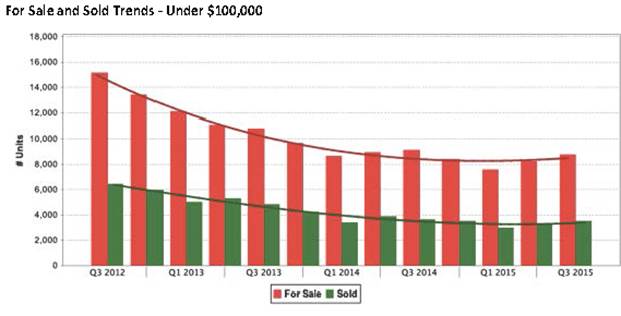

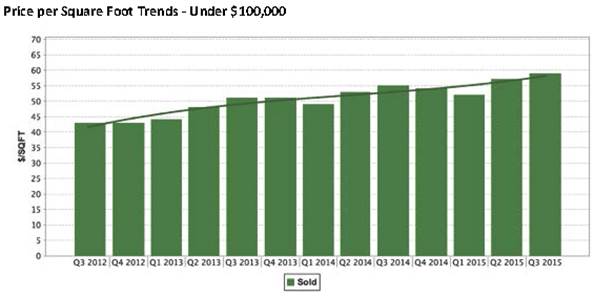

The under $100,000 market has shown a steady decline in sales and inventory over the past three years as a result of fewer bank-owned homes. Removing the bank-owned properties, the number of sales are down only slightly and the number of listings are actually rising over the past 2 quarters. Values based on the average price per square foot have had a steady rise, the most of any price point, as a result of both fewer lower priced bank-owned properties and more buyers competing for fewer listings.

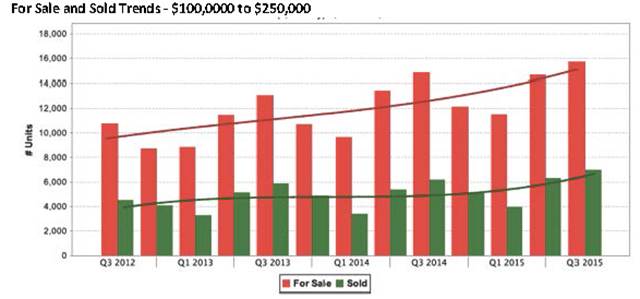

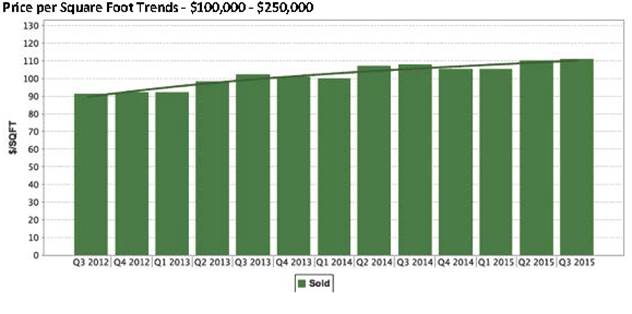

The next price point, $100k to $250k, shows a more pronounced rise in inventory, along with a strong jump in sales, with the rise in inventory since mid-2014 out pacing the rise in sales which has resulted in a corresponding flattening of the increase in value per square foot during 2015. We expect these trends to continue through the fall and winter, keeping values relatively flat.

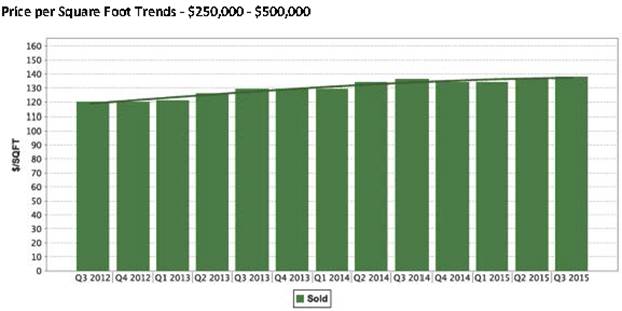

The $250k to $500k price points follow the same trends as the prior charts with a more pronounced increased in listing inventory this year which results in an even flatter pricing chart for 2015.

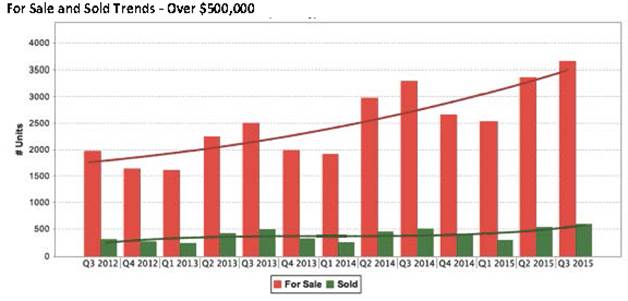

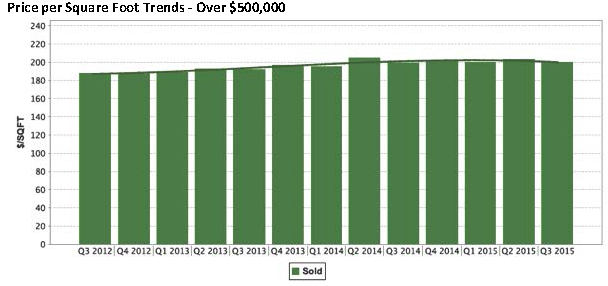

For the luxury market, the gap between the rise in inventory and sales has been the most pronounced, so it has not been surprising to see values remain flat, and even start to decline, during this past quarter. We don’t expect this value decline to be a long-term trend, but until inventories are absorbed later in 2016, values will remain flat, or in some cases, continue to decline.

All investment markets, whether stocks or real estate, don’t recover in a steady line, they jump around as demand jumps, then supply follows, then demand jumps again. So for the next year or so, across all price points, we should see a temporary jump in For Sale inventory, and over the balance of 2016, the market should settle back down to a better balance as those new listings are sold.

Enjoy the great fall colors and a new fall home as well!